31 Aralık 2012 Pazartesi

President rejects his bipartisan commission

The fiscal deal struck last night makes one thing clear: President Obama must have really hated the recommendations of the bipartisan Bowles-Simpson commission that he appointed. The commission said that we needed to reform entitlement programs to rein in spending and that increased tax revenue should come in the form of base broadening and lower marginal tax rates. The deal appears to offer no entitlement reforms, no tax reform, and higher marginal tax rates. After all the public discussion over the past couple years of what a good fiscal reform would look like, it is hard to imagine a deal that would be less responsive to the ideas of bipartisan policy wonks.

The Neverending Quest for a More Redistributionist Tax System

I just listened to President Obama's latest remarks on fiscal policy. This passage caught my attention:

Translation: The deal we are about to strike will raise taxes on the rich. But the fiscal imbalances we face will remain unsustainably large. So I will ask for more tax increases on the rich later.

I want to make clear that any agreement we have to deal with these automatic spending cuts that are being threatened for next month, those also have to be balanced, because, remember, my principle always has been let’s do things in a balanced, responsible way. And that means the revenues have to be part of the equation in turning off the sequester and eliminating these automatic spending cuts, as well as spending cuts.

Now, the same is true for any future deficit agreement. Obviously we’re going to have to do more to reduce our debt and our deficit. I’m willing to do more, but it’s going to have to be balanced. We’re going to have do it in a balanced responsible way.

For example, I’m willing to reduce our government’s Medicare bills by finding new ways to reduce the cost of health care in this country. That’s something that we all should agree on. We want to make sure that Medicare is there for future generations. But the current trajectory of health care costs has gone up so high, we’ve got to find ways to make sure that it’s sustainable.

But that kind of reform has to go hand and hand with doing some more work to reform our tax code, so that wealthy individuals, the biggest corporations, can’t take advantage of loopholes and deductions that aren’t available to most of the folks standing up here; aren’t available to most Americans.

So there is still more work to be done in the tax code to make it fair, even as we’re also looking at how we can strengthen something like Medicare.

Translation: The deal we are about to strike will raise taxes on the rich. But the fiscal imbalances we face will remain unsustainably large. So I will ask for more tax increases on the rich later.

Are long-run incentive going to ruin healthcare reform in the US?

Insurance is a horribly complicated concept. While it provides benefits by preventing to a large extend the consequences of adverse shocks, it can also lead to sometimes severe moral hazard. Car insurance can lead to more dangerous driving. Health insurance can lead to more risky behavior. It is thus not obvious that introducing insurance is on the whole beneficial, especially if premiums cannot reflect risk.

Harold Cole, Soojin Kim and Dirk Krueger do such a welfare analysis for the upcoming US health insurance scheme. While there is a clear benefit in the short term, current conditions not having been perverted by the presence of insurance, the welfare outcome in the long-run needs to be determined once people have adjusted their behavior. They find that the negative impact of uniform insurance is severely amplified if other consequences of poor health choices are prevented from occurring, in their example prohibition of wage discrimination against workers with poor health. They find that this effect is so strong that cohorts become gradually of poorer health and overcome the positive impact of insurance stricto sensu. This means we need to incentivize good behavior, an example being sin taxes that have been the subject of several recent blog posts here.

Harold Cole, Soojin Kim and Dirk Krueger do such a welfare analysis for the upcoming US health insurance scheme. While there is a clear benefit in the short term, current conditions not having been perverted by the presence of insurance, the welfare outcome in the long-run needs to be determined once people have adjusted their behavior. They find that the negative impact of uniform insurance is severely amplified if other consequences of poor health choices are prevented from occurring, in their example prohibition of wage discrimination against workers with poor health. They find that this effect is so strong that cohorts become gradually of poorer health and overcome the positive impact of insurance stricto sensu. This means we need to incentivize good behavior, an example being sin taxes that have been the subject of several recent blog posts here.

29 Aralık 2012 Cumartesi

The year ahead

It is not my style to opine on current events, and especially not to forecast. Yet, seems that there are some general trends that are worth mentioning that may not have been stated enough. So here we go with my take about what lies ahead.

Latin America

Latin America has done remarkably well lately, especially considering developed economies were not. Even more remarkable is the very rapid income growth of the poor population leading to a rapid reduction in inequality. There is still a lot of potential and things look good. Of course, the region is always good for bad political surprises.

Asia

This is a big continent, so it is difficult to generalize. Its economy has grown tremendously in the past years and this will continue. Unfortunately, there are risks. May a housing bubble burst in China? Will the very large number of underprivileged in China ask for its fair share of the new riches? Can India continue its liberalization? Contrast this with long-stagnating Japan, whose new government wants to get the economy kicking again by creating inflation (it is not clear how the government can do that). And politics will continue to dominate economic affairs in the western part of the continent.

Europe

Europe is a mess, and mostly of its own doing. Undoing this is not going to be easy, as credibility needs to be rebuilt. This is going to be another nerve-wracking year with empty promises. Greece will continue in its corrupt ways, inexplicably dragging everybody with it (and possibly collapsing for the second time a currency union). Italy will go through unnecessary instability thanks to Berlusconi again, and the French government will listen to the street instead of the experts. Watch out also for Norway, Sweden and Switzerland, where housing bubbles may burst. And Germany will continue posturing and lecturing the others, while everybody ignores the UK (and Russia, too).

North America

Speaking of unnecessary posturing, the US is the poster child right now. Republicans are hoping taxes will go up with the "fiscal cliff" and claim it is not their fault, then negotiate a compromise with taxes at midpoint and claim victory thanks to lowered taxes. And what did we gain from this? Uncertainty, frustration and unnecessary distractions. And unless Democrats (and the President) finally take a strong stand, politics will remain in flux and threaten a nascent recovery. Canada will watch all this, shake its head and go on, hoping for the best.

Africa

What to think of Africa? It is going to remain a basket case, with a few hopes that are quickly dashed. Rebels will be disrupting the normal course of things in several countries, corruption and rent-seeking will remain the principal industry, and foreign aid will continue to be wasted. Let us hope that manufacturing will finally take off on a continent that is not made for agriculture.

In summary

Politics will continue messing with economies (and economists).

Latin America

Latin America has done remarkably well lately, especially considering developed economies were not. Even more remarkable is the very rapid income growth of the poor population leading to a rapid reduction in inequality. There is still a lot of potential and things look good. Of course, the region is always good for bad political surprises.

Asia

This is a big continent, so it is difficult to generalize. Its economy has grown tremendously in the past years and this will continue. Unfortunately, there are risks. May a housing bubble burst in China? Will the very large number of underprivileged in China ask for its fair share of the new riches? Can India continue its liberalization? Contrast this with long-stagnating Japan, whose new government wants to get the economy kicking again by creating inflation (it is not clear how the government can do that). And politics will continue to dominate economic affairs in the western part of the continent.

Europe

Europe is a mess, and mostly of its own doing. Undoing this is not going to be easy, as credibility needs to be rebuilt. This is going to be another nerve-wracking year with empty promises. Greece will continue in its corrupt ways, inexplicably dragging everybody with it (and possibly collapsing for the second time a currency union). Italy will go through unnecessary instability thanks to Berlusconi again, and the French government will listen to the street instead of the experts. Watch out also for Norway, Sweden and Switzerland, where housing bubbles may burst. And Germany will continue posturing and lecturing the others, while everybody ignores the UK (and Russia, too).

North America

Speaking of unnecessary posturing, the US is the poster child right now. Republicans are hoping taxes will go up with the "fiscal cliff" and claim it is not their fault, then negotiate a compromise with taxes at midpoint and claim victory thanks to lowered taxes. And what did we gain from this? Uncertainty, frustration and unnecessary distractions. And unless Democrats (and the President) finally take a strong stand, politics will remain in flux and threaten a nascent recovery. Canada will watch all this, shake its head and go on, hoping for the best.

Africa

What to think of Africa? It is going to remain a basket case, with a few hopes that are quickly dashed. Rebels will be disrupting the normal course of things in several countries, corruption and rent-seeking will remain the principal industry, and foreign aid will continue to be wasted. Let us hope that manufacturing will finally take off on a continent that is not made for agriculture.

In summary

Politics will continue messing with economies (and economists).

28 Aralık 2012 Cuma

There is no such thing as a real economy

Nothing beats a well-written abstract. You want in particular to use the right terminology, state clearly what you want to do and given a few good hints about your conclusions. A confusing abstract is a real put-off, but they do happen. They usually signal a really bad paper, and the chances that there is interesting content behind the veil of a obfuscating presentation is slim. Take this one:

This is the work of Egmont Kakarot-Handtke, whose paper mirrors the abstract. It hinges on absurd assumptions which are not justified in any way, and some sort of logic is applied from there. For example, it is stated as a basic premise that profits are not real, only monetary, and this was completely overlooked by all economists. I wonder how economies worked before the introduction of money. The paper continues with "axioms" which are in fact three definitions, whose equations do not share a single variable, and a law of motion for yet another variable. After seeing how prices are determined by accounting identities, I stopped reading. Yet, I somehow felt compelled to write this. It must be the holiday spirit.

There is no such thing as a real economy. The task, therefore, is to consistently reconstruct the fluctuations of employment and output from the interactions of real and nominal variables. The present paper does exactly this. No nonempirical concepts like utility, equilibrium, rationality, decreasing returns or perfect competition are applied. The analysis runs rigorously in objective structural axiomatic terms. Therefrom follows that it is the factor cost ratio, i.e. the relation of the nominal variables wage rate and price and the real variable productivity that, for any given level of effective demand, drives the fluctuations of employment and output.

This is the work of Egmont Kakarot-Handtke, whose paper mirrors the abstract. It hinges on absurd assumptions which are not justified in any way, and some sort of logic is applied from there. For example, it is stated as a basic premise that profits are not real, only monetary, and this was completely overlooked by all economists. I wonder how economies worked before the introduction of money. The paper continues with "axioms" which are in fact three definitions, whose equations do not share a single variable, and a law of motion for yet another variable. After seeing how prices are determined by accounting identities, I stopped reading. Yet, I somehow felt compelled to write this. It must be the holiday spirit.

Theater Recommendation

For those in the Boston area: Yesterday, my family and I enjoyed one of our Christmas presents from Santa and went to the new production of the musical Pippin at the American Repertory Theater in Cambridge. I recall seeing the original Broadway production in the 1970s when I was in high school and liking the play then. I went to see it yesterday with a bit of trepidation, wondering whether my sensibilities had changed too much over the past four decades for me to still enjoy it. But the play did not disappoint, not even one bit. This new production is absolutely terrific: great acting, music, dancing, and even acrobatics. Everyone had a blast, from my teenage sons to my 85-year-old mother.

The play's run lasts until January 20. Go see it if you can.

The play's run lasts until January 20. Go see it if you can.

27 Aralık 2012 Perşembe

European tourism and the Euro

If you have traveled across Europe before the introduction of the Euro, you have certainly been annoyed by the frequent changing of currencies. Not only did you need to worry about getting cash at the border, you also had tp learn about new denominations, rethink the prices you see, and end up with unused loose change (ignoring the exchange risk one faces as well). With the introduction of the Euro, all this has been greatly simplified, even if not all countries joined. Beyond the convenience for the tourist, has this spurred additional tourism.

María Santana Gallego, Jorge Vicente Pérez Rodríguez and Francisco Jos&e;eacut Ledesma Rodríguez ask this question and find that, yes, it had a positive impact, to the tune of 20 to 40% for EMU country tourist arrivals, and mostly so after 2002 (when Euro coins and notes were introduced) in contrast to 1999 (when the exchange rates were fixed). In addition, there is evidence of tourism diversion: The stated increases occurred to the detriment of non-EMU countries. In other words, tourists substituted away from countries that are not carrying the Euro.

PS: Things seem to be looking a bit better for Greece right now. But if it were still to be dropped from the Euro-zone, consider a substantial negative impact on its vital tourism industry.

María Santana Gallego, Jorge Vicente Pérez Rodríguez and Francisco Jos&e;eacut Ledesma Rodríguez ask this question and find that, yes, it had a positive impact, to the tune of 20 to 40% for EMU country tourist arrivals, and mostly so after 2002 (when Euro coins and notes were introduced) in contrast to 1999 (when the exchange rates were fixed). In addition, there is evidence of tourism diversion: The stated increases occurred to the detriment of non-EMU countries. In other words, tourists substituted away from countries that are not carrying the Euro.

PS: Things seem to be looking a bit better for Greece right now. But if it were still to be dropped from the Euro-zone, consider a substantial negative impact on its vital tourism industry.

Glaeser on Disability

Ed considers what might be behind this fact:

Thirty years ago, there was a 40-to-1 ratio between the total labor force and those workers receiving Social Security disability payments. Today that ratio is less than 18-to-1.

24 Aralık 2012 Pazartesi

A Reading for Christmas

My favorite Christmas-themed economics article is this one by Steve Landsburg. From 2004, but truly timeless.

The economics of yoga

I appreciate yoga because it helps my stiff body to loosen up, and because it forces me to take some time off the multiple things I do to calm down. But I would not call this meditation, although many people do. I chat during the moves, thus for me it is a purely physical experience. Many others do it for the opportunity to free up and "purify" your mind, although I have been suspicious about such claims. It would take me an economist to convince me otherwise, and maybe the following study does.

Giovanni Di Bartolomeo, Stefano Papa and Saverio Bellomo look at how yoga and supposed meditation changes the way people trust each other and cooperate. They exposed some participants to yoga meditation (with Tibetan singing bowls no less) before an investment experiment. The "pre-meditated" participants showed lower risk aversion and more trust than the non-exposed ones. I wonder how this small experiment would scale up. Do countries with cultures based on meditation also have higher levels of trust and risk tolerance? Do they have institutions that rely more on trust? Something to ponder over the holidays.

Giovanni Di Bartolomeo, Stefano Papa and Saverio Bellomo look at how yoga and supposed meditation changes the way people trust each other and cooperate. They exposed some participants to yoga meditation (with Tibetan singing bowls no less) before an investment experiment. The "pre-meditated" participants showed lower risk aversion and more trust than the non-exposed ones. I wonder how this small experiment would scale up. Do countries with cultures based on meditation also have higher levels of trust and risk tolerance? Do they have institutions that rely more on trust? Something to ponder over the holidays.

A Krugman Puzzler

I often disagree with Paul Krugman, but I usually understand him. Lately, however, I have been puzzled about his view of the bond market. In a recent post, he takes President Obama to task for believing that the failure to deal with our long-term fiscal imbalance might cause a spike in interest rates:

But back in 2003, when the fiscal imbalance was much smaller, he wrote:

Update: Several people have emailed me possible resolutions of the puzzle, but none is really satisfying.

One group of emailers says that things are different now because we are in a liquidity trap. But back in 2003 the federal funds rate was at about 1 percent, so we were very close to the zero lower bound.

Another group of emailers says that Paul has admitted that his 2003 forecast was mistaken. But that is not the issue. Of course, we can look back and say it was mistaken. No big deal. Any economist who has ever made a forecast has made some mistaken forecasts. The puzzle to me is how Paul can act so certain that the outcome he viewed as likely in 2003 is now beyond the realm of the plausible, even though the fiscal imbalances are much larger.

By the way, my column coming out in Sunday's NY Times touches on these issues, which is why the puzzle came to mind.

America can’t run out of cash (except politically, if Congress refuses to raise the debt ceiling); it basically can’t experience an interest rate spike unless people see an increased chance of economic recovery and hence a rise in short-term rates. And the people who have been predicting an interest rate spike any day now for four years shouldn’t have any credibility at this point.

But back in 2003, when the fiscal imbalance was much smaller, he wrote:

With war looming, it's time to be prepared. So last week I switched to a fixed-rate mortgage. It means higher monthly payments, but I'm terrified about what will happen to interest rates once financial markets wake up to the implications of skyrocketing budget deficits....

How will the train wreck play itself out? Maybe a future administration will use butterfly ballots to disenfranchise retirees, making it possible to slash Social Security and Medicare. Or maybe a repentant Rush Limbaugh will lead the drive to raise taxes on the rich. But my prediction is that politicians will eventually be tempted to resolve the crisis the way irresponsible governments usually do: by printing money, both to pay current bills and to inflate away debt.

And as that temptation becomes obvious, interest rates will soar. It won't happen right away. With the economy stalling and the stock market plunging, short-term rates are probably headed down, not up, in the next few months, and mortgage rates may not have hit bottom yet. But unless we slide into Japanese-style deflation, there are much higher interest rates in our future.

I think that the main thing keeping long-term interest rates low right now is cognitive dissonance. Even though the business community is starting to get scared -- the ultra-establishment Committee for Economic Development now warns that ''a fiscal crisis threatens our future standard of living'' -- investors still can't believe that the leaders of the United States are acting like the rulers of a banana republic. But I've done the math, and reached my own conclusions -- and I've locked in my rate.I am having trouble reconciling these points of views. Has Paul changed his mind since 2003 about how the bond market works? Or are circumstances different now? If anything, I would have thought that the fiscal situation is more dire now and so the logic from 2003 would apply with more force. I am puzzled.

Update: Several people have emailed me possible resolutions of the puzzle, but none is really satisfying.

One group of emailers says that things are different now because we are in a liquidity trap. But back in 2003 the federal funds rate was at about 1 percent, so we were very close to the zero lower bound.

Another group of emailers says that Paul has admitted that his 2003 forecast was mistaken. But that is not the issue. Of course, we can look back and say it was mistaken. No big deal. Any economist who has ever made a forecast has made some mistaken forecasts. The puzzle to me is how Paul can act so certain that the outcome he viewed as likely in 2003 is now beyond the realm of the plausible, even though the fiscal imbalances are much larger.

By the way, my column coming out in Sunday's NY Times touches on these issues, which is why the puzzle came to mind.

23 Aralık 2012 Pazar

21 Aralık 2012 Cuma

Sin taxes and liberty

I have discussed quite a few times sin taxes that are instituted to redress some individual behavior. Indeed, people make choices that harm others or themselves directly or indirectly. They create congestion and pollution by driving a care, they increase tax- or insurance-financed health care cost by smoking or becoming obese, they also become public hazards by being drunk. This is one reason why we often tax automotive fuels, unhealthy foods, tobacco and alcohol more than other goods.

But some people object to such sin taxes because they infringe on personal liberties. One of them is Gilles Saint-Paul, whose work I have several times discussed here in a positive light (I, II, III), but this time I have to disagree. His view is that the state is too paternalistic when it intervenes in otherwise free markets with sin taxes, and this has become worse since behavioral economics has highlighted choice patterns that deviate from standard utilitarianism. Well, this is exactly the point. Behavioral economics has brought forward that there are situations were people take actions that they later regret. This is precisely when they would appreciate (at least later) some paternalism in the sense that the state can provide them with a commitment device.

So why does Saint-Paul object to this? His argument is that one should not object to personal choices, and that people should only blame themselves for poor choices. But what if one can help them? Should this not happen only because it is the state? He complains that economists have abandoned utilitarism, which maximizes the sum of individual utilities. I do not think that is correct, but he seems to completely ignore that there are externalities out there, that there is regret, that there are temptations, and that there is lack of commitment. and all this should not be myopically ignored when computing utilities. He is going as far as comparing this supposed abandonment of utilitarianism to eugenics. In other words, he sees excessive government intervention. I agree that there is potential for this, but I see no demonstration that this is happening, and the mere fact that there is intervention is not sufficient, as Saint-Paul seems to imply in a rather puzzling paper.

PS: Robert Wiblin at Overcoming Bias has recently made a similar argument to libertarians in favor of paternalism and also finds it "incredibly obvious." Yet, it needs to be made.

But some people object to such sin taxes because they infringe on personal liberties. One of them is Gilles Saint-Paul, whose work I have several times discussed here in a positive light (I, II, III), but this time I have to disagree. His view is that the state is too paternalistic when it intervenes in otherwise free markets with sin taxes, and this has become worse since behavioral economics has highlighted choice patterns that deviate from standard utilitarianism. Well, this is exactly the point. Behavioral economics has brought forward that there are situations were people take actions that they later regret. This is precisely when they would appreciate (at least later) some paternalism in the sense that the state can provide them with a commitment device.

So why does Saint-Paul object to this? His argument is that one should not object to personal choices, and that people should only blame themselves for poor choices. But what if one can help them? Should this not happen only because it is the state? He complains that economists have abandoned utilitarism, which maximizes the sum of individual utilities. I do not think that is correct, but he seems to completely ignore that there are externalities out there, that there is regret, that there are temptations, and that there is lack of commitment. and all this should not be myopically ignored when computing utilities. He is going as far as comparing this supposed abandonment of utilitarianism to eugenics. In other words, he sees excessive government intervention. I agree that there is potential for this, but I see no demonstration that this is happening, and the mere fact that there is intervention is not sufficient, as Saint-Paul seems to imply in a rather puzzling paper.

PS: Robert Wiblin at Overcoming Bias has recently made a similar argument to libertarians in favor of paternalism and also finds it "incredibly obvious." Yet, it needs to be made.

20 Aralık 2012 Perşembe

The short-run impact of taxing saturated fats

Saturated fats are bad, and we should avoid them. But they are cheaper than non-saturated fats, and if they are that bad, the obvious solution is to impose a tax on the bad ones so that they become more expensive than the good ones. Or you could inform users so that they make the best choice, but you still need to tax if the consumption of bad fats has an impacts on others, as in increased demand for health care that is paid at least in part by public funds. One way or the other, you need to tax saturated fats. The question is how much do you need to tax, and before answering that question you need to know how responsive people are to such taxes.

Jørgen Dejgård Jensen and Sinne Smed study this last question for Denmark, where a tax was introduced in October 2011. That was very recently, so they can only figure out the short-term elasticity. They find that for the products containing the most saturated fats, such as butter and oils, quantities sold decreased by 10-20% for an increase of tax in the order of 8 to 22% (it varies because the nutrient is taxed, not the food class). That looks a significant elasticity for foods that are quite essential to cooking. But as I mentioned in the introduction, another way of reduction consumption of "bad" foods is to inform the public. I suspect this what also happened with the introduction of this tax, as the media must have written about it and made many people aware of the adversarial effects of saturated fats. With the current empirical strategy, there is no way the authors can identify the impact of the tax from the impact of information, and that is likely why the elasticity is so high.

Jørgen Dejgård Jensen and Sinne Smed study this last question for Denmark, where a tax was introduced in October 2011. That was very recently, so they can only figure out the short-term elasticity. They find that for the products containing the most saturated fats, such as butter and oils, quantities sold decreased by 10-20% for an increase of tax in the order of 8 to 22% (it varies because the nutrient is taxed, not the food class). That looks a significant elasticity for foods that are quite essential to cooking. But as I mentioned in the introduction, another way of reduction consumption of "bad" foods is to inform the public. I suspect this what also happened with the introduction of this tax, as the media must have written about it and made many people aware of the adversarial effects of saturated fats. With the current empirical strategy, there is no way the authors can identify the impact of the tax from the impact of information, and that is likely why the elasticity is so high.

19 Aralık 2012 Çarşamba

How randomized experiments can go very wrong

Randomized experiments are all the rage in some circles, for example labor economics and especially development economics. The principle is simple: create some intervention in some market, randomly draw a group of economic agents that has access to the intervention, leave the others out, compare outcomes. In all that, you hope the behavior of the non-participants is not affected by the presence of the program to the others. This can be a heroic assumption, for example because market prices may respond for everyone to the intervention.

Pieter Gautier, Paul Muller, Bas van der Klaauw, Michael Rosholm and Michael Svarer show an example where this assumption was violated. The intention was to see how helping Danish unemployed workers find jobs through enhanced guidance was successful. Those who were non-selected had to deal with the job search as usual. In that case, there were some regions where the experiment was not conducted but data still collected. In the two counties where the experiment was conducted, the number of vacancies markedly increased, which logically leads the treated and untreated to have a better shot at finding a job. But, of course, there is also a congestion effect: for the same number of vacancies, if some workers are getting better probabilities for finding jobs, it is getting worse for the others. In the Danish case, overall this turned out to get worse for the non-participants.

Several papers had previously looked at this experiment and concluded the intervention was a great success because participants fared so much better. But the result can of course not be generalized. What if everyone searches more for the same number of vacancies? Nothing changes much, except that vacancies may be filled faster. And what if the number of vacancies increased in those two counties because of the treatment, to the detriment of the other counties? Then applying the program to the whole country should not make a difference. Given the cost of these studies, this is a very disappointing result.

Pieter Gautier, Paul Muller, Bas van der Klaauw, Michael Rosholm and Michael Svarer show an example where this assumption was violated. The intention was to see how helping Danish unemployed workers find jobs through enhanced guidance was successful. Those who were non-selected had to deal with the job search as usual. In that case, there were some regions where the experiment was not conducted but data still collected. In the two counties where the experiment was conducted, the number of vacancies markedly increased, which logically leads the treated and untreated to have a better shot at finding a job. But, of course, there is also a congestion effect: for the same number of vacancies, if some workers are getting better probabilities for finding jobs, it is getting worse for the others. In the Danish case, overall this turned out to get worse for the non-participants.

Several papers had previously looked at this experiment and concluded the intervention was a great success because participants fared so much better. But the result can of course not be generalized. What if everyone searches more for the same number of vacancies? Nothing changes much, except that vacancies may be filled faster. And what if the number of vacancies increased in those two counties because of the treatment, to the detriment of the other counties? Then applying the program to the whole country should not make a difference. Given the cost of these studies, this is a very disappointing result.

18 Aralık 2012 Salı

Do state scholarships keep graduates in the state?

Many US states provide special study scholarships reserved to state residents which be applied to any in-state university, including private ones. This goes beyond the lower tuitions at state universities for state residents. The idea is that students tend to stay for work (and pay taxes and improve human capital) where they studied, thus you want to get them to study in-state. If every state does this, the macroeconomic impact is zero on work location, no matter what the mobility, and negative on state budgets. But this is a game hat states play, like they do with tax competition, thus it is interesting to see whether a state gains from playing this if all others already do.

Maria Fitzpatrick and Damon Jones find that the impact of these programs can be found, but it is quite small. That money is thus mostly going to either students who move out-of-state after their studies or to students who would have stayed within state boundaries anyway. This result is obtained by looking at the expansion of these program in 15 states from 1990 to 2010 and how they impacted residential patterns. It would of course be better to have information from the students themselves (and a control group), but you got to start somewhere.

Maria Fitzpatrick and Damon Jones find that the impact of these programs can be found, but it is quite small. That money is thus mostly going to either students who move out-of-state after their studies or to students who would have stayed within state boundaries anyway. This result is obtained by looking at the expansion of these program in 15 states from 1990 to 2010 and how they impacted residential patterns. It would of course be better to have information from the students themselves (and a control group), but you got to start somewhere.

17 Aralık 2012 Pazartesi

Limit gas price changes to once a day?

For some reason that is unclear to me, fuel for cars is in most countries the most flexible price, sometimes changing several times a day. As demand is rather inelastic and the raw commodity supply comes from politically volatile regions, the price also fluctuates over a wide range. And this wide range leads to a lot of grief, especially when prices go up, with calls from the public for politicians to do something about it. The latter then usually do something stupid, and they are never short of ideas.

One recent innovation comes from Austria: in the belief that higher prices come from frequent changes, gas stations have been limited to one price change a day. Martin Obradovits analyzes this policy and comes to the obvious an obvious answer: it is a stupid policy. For one, it is not like gas companies are bound by fixed increments and this would reduce fluctuations. Second, it introduces new frictions in the market that go to the detriment of the consumer: you get the same profits and the same expense for the same quantities, there is only some intertemporal rejuggling that inconveniences the buyers. I would add that if prices end up too low during the day, gas stations may simply close and ration out buyers until they can adjust prices. Ah, politicians...

One recent innovation comes from Austria: in the belief that higher prices come from frequent changes, gas stations have been limited to one price change a day. Martin Obradovits analyzes this policy and comes to the obvious an obvious answer: it is a stupid policy. For one, it is not like gas companies are bound by fixed increments and this would reduce fluctuations. Second, it introduces new frictions in the market that go to the detriment of the consumer: you get the same profits and the same expense for the same quantities, there is only some intertemporal rejuggling that inconveniences the buyers. I would add that if prices end up too low during the day, gas stations may simply close and ration out buyers until they can adjust prices. Ah, politicians...

16 Aralık 2012 Pazar

15 Aralık 2012 Cumartesi

Five years of blogging

The Economic Logic blog is now five years old. At every anniversary, I reevaluate whether it is worth continuing in this effort. After all, there is little reward in blogging anonymously, rather the opposite, and writing here competes with my real world duties. And it has become more difficult since I took on some new responsibilities (some readers may have noticed that my posts were sometimes a bit short). However, readership has been steadily increasing and I have some sense of duty to keep posting. Stopping now cold turkey would definitely leave me empty. But I may consider skipping days here and there when my real world duties keep me away from my "second life."

So, I will keep posting for another year. There is still a lot of interesting research going on in Economics. And there is still a lot of papers that may not get published in the best journals but merit mentions because they have interesting implications. And sometimes there are some really bad papers that need to be pointed out before they do more damage.

Traditionally, I have pointed out with posts were the most read during the last year. For a variety of reasons, I can only find the three that were posted during 2012. By far the most popular was a very recent post, "How to make your children intelligent". The two next were "The Harvard Economics Department's Nobel problem" and "Mathematics, Econometrics and top economists' career outcomes".

I hope you will read Economic Logic for another year. I will be there.

So, I will keep posting for another year. There is still a lot of interesting research going on in Economics. And there is still a lot of papers that may not get published in the best journals but merit mentions because they have interesting implications. And sometimes there are some really bad papers that need to be pointed out before they do more damage.

Traditionally, I have pointed out with posts were the most read during the last year. For a variety of reasons, I can only find the three that were posted during 2012. By far the most popular was a very recent post, "How to make your children intelligent". The two next were "The Harvard Economics Department's Nobel problem" and "Mathematics, Econometrics and top economists' career outcomes".

I hope you will read Economic Logic for another year. I will be there.

14 Aralık 2012 Cuma

Complicated auctions are more proftable

There was a time where auction theory limited itself to studying very simple auction, where the subtleties were whether the first or second price should be paid (or the first less an increment). Now, auction theory looks at much more complex mechanisms, for example where bidders may or may not reveal their bids, or whether they are bidding, or where bidding comes with a fix price. Not all these mechanisms try to obtain a surplus maximizing outcome. Some maximize the profits of the seller, sometimes by confusing or even misleading the seller. The most extreme example are penny auctions, about which I posted before (I, II).

Andrea Gallice discusses a variation of the Dutch auction where the current winning bid price remains hidden but can be observed against a fee. This so-called price reveal auction has an additional twist: paying that fee makes the winning bid fall by a predetermined amount. An auction so complex must be designed to maximize someone's surplus. It is the seller. And his profits are even higher if he manages to keep the number of bidders secret. This is not unlike penny auctions, where the profits come from the fees, not the winning bid.

OK, this maximizes profits, but I do not think this maximizes overall well-being. Obfuscation is not likely to be beneficial, and I am quite surprised the author does not address this. Until convinced of the contrary, I am going to assume that such obfuscation is detrimental for society and should be outlawed. And with rules so complex, it would not surprise me that bidders would have a hard time behaving rationally.

Andrea Gallice discusses a variation of the Dutch auction where the current winning bid price remains hidden but can be observed against a fee. This so-called price reveal auction has an additional twist: paying that fee makes the winning bid fall by a predetermined amount. An auction so complex must be designed to maximize someone's surplus. It is the seller. And his profits are even higher if he manages to keep the number of bidders secret. This is not unlike penny auctions, where the profits come from the fees, not the winning bid.

OK, this maximizes profits, but I do not think this maximizes overall well-being. Obfuscation is not likely to be beneficial, and I am quite surprised the author does not address this. Until convinced of the contrary, I am going to assume that such obfuscation is detrimental for society and should be outlawed. And with rules so complex, it would not surprise me that bidders would have a hard time behaving rationally.

13 Aralık 2012 Perşembe

Why corruption will always be with us

How would one define corruption. In economic terms, one definition could that two parties engage in a mutually beneficial transaction to the detriment of an other and society in general, and this despite rules put in place to prevent this. I am not sure everyone will agree with this definition, as it includes everyday situations that one may not generally associate with corruption, such as small gifts we offer to superiors or teachers.

Ulrike Malmendier and Klaus Schmidt study, without calling it corruption, such behavior in an experimental setting. They find that subjects of a gift do reciprocate even if they have no incentive to do so. Worse, they reciprocate more if it is at the expense of a third party, and everybody knows that the third party is affected. Finally, participants correctly assess how their behavior was influenced by gifts, but believe others are much more influenced. It is difficult to square any standard theory with these results. It also implies that such gift-giving is going to be difficult to stamp out, at least when it is relatively small such as in these experiments.

Ulrike Malmendier and Klaus Schmidt study, without calling it corruption, such behavior in an experimental setting. They find that subjects of a gift do reciprocate even if they have no incentive to do so. Worse, they reciprocate more if it is at the expense of a third party, and everybody knows that the third party is affected. Finally, participants correctly assess how their behavior was influenced by gifts, but believe others are much more influenced. It is difficult to square any standard theory with these results. It also implies that such gift-giving is going to be difficult to stamp out, at least when it is relatively small such as in these experiments.

Interpreting the Fed

My friend and sometime coauthor Larry Ball sends me his quick analysis of the Federal Reserve's recent announcement:

I think the FOMC announcement is big news: for the first time, the Fed clearly says it will be more dovish in the future than the pre-crisis Taylor Rule (TR) dicates.

In my estimation, the pre-crisis TR is something like the following for the real interest rate r:

r = 2.0 - (1.5)(u-u*) + (0.5)(pi-2.0).

Let’s say u* is still 5.0. Then if u=6.5 and pi=2.5, the TR says r = 0, which implies the nominal interest rate is i = 2.5. Yet the Fed says that i will still be zero!

Some argue that u* has risen above 5.0. That would raise the i implied by the TR, strengthening the conclusion that the Fed’s new rule is more dovish than the TR.

Some argue that r* [the constant term in the TR] has fallen from 2.0 to 1.0. I doubt it, but even with that change, the TR still implies i = 1.5. My conclusion about dovishness is robust.

This deviation from the TR has not happened since the TR was discovered. In particular, the Fed was NOT more dovish than the TR in 2003. I believe the numbers for 2003 are roughly u=6.0, u*=5.0, and pi=1.0. For the TR shown above, the 2003 numbers imply r =0 and i=1.0, which is about the same as the actual i.

It is not clear whether the Fed’s announcement of future dovishness will have significant effects today. The efficacy of announcements about future monetary policy is unproven.

I think the FOMC announcement is big news: for the first time, the Fed clearly says it will be more dovish in the future than the pre-crisis Taylor Rule (TR) dicates.

In my estimation, the pre-crisis TR is something like the following for the real interest rate r:

r = 2.0 - (1.5)(u-u*) + (0.5)(pi-2.0).

Let’s say u* is still 5.0. Then if u=6.5 and pi=2.5, the TR says r = 0, which implies the nominal interest rate is i = 2.5. Yet the Fed says that i will still be zero!

Some argue that u* has risen above 5.0. That would raise the i implied by the TR, strengthening the conclusion that the Fed’s new rule is more dovish than the TR.

Some argue that r* [the constant term in the TR] has fallen from 2.0 to 1.0. I doubt it, but even with that change, the TR still implies i = 1.5. My conclusion about dovishness is robust.

This deviation from the TR has not happened since the TR was discovered. In particular, the Fed was NOT more dovish than the TR in 2003. I believe the numbers for 2003 are roughly u=6.0, u*=5.0, and pi=1.0. For the TR shown above, the 2003 numbers imply r =0 and i=1.0, which is about the same as the actual i.

It is not clear whether the Fed’s announcement of future dovishness will have significant effects today. The efficacy of announcements about future monetary policy is unproven.

12 Aralık 2012 Çarşamba

Japan's lost demographic decades

Since the asset bubble burst in Japan in 1990, the economy has stagnated despite significant policy efforts. Interest rates have been very low all along and fiscal policy has certainly not been austere. What was once labeled a lost decade has now become a pair of lost decades. Can only the burst bubble and the issues with the Japanese financial system be blamed?

Reiko Aoki thinks the demographic change in Japan has a large role in this extended stagnation. As is well know, Japan is aging considerably, and this has of course a dramatic impact of the savings picture. Financial institutions that were built to accommodate rapid growth and a young population looking to safeguard massive amounts of savings struggle to deal a much older population that is in the phase of eating its savings. Worse, as institutions need to adapt to the new situation, reform is hindered by the large voting block of the elderly whose interest lies in the short-term provision of their pensions.

Quite obviously, the current imbalance in the demographic pyramid is the problem. Aoki thinks that fertility must be encouraged. This has worked little in other economies, but may be much easier to implement politically than the best solution, get people to retire later. Immigration is another solution, but as other countries are looking to embrace similar solutions, we may run out of willing young migrants. And Japan is not the obvious choice for a migrant, given the high entry cost in terms of integration.

Reiko Aoki thinks the demographic change in Japan has a large role in this extended stagnation. As is well know, Japan is aging considerably, and this has of course a dramatic impact of the savings picture. Financial institutions that were built to accommodate rapid growth and a young population looking to safeguard massive amounts of savings struggle to deal a much older population that is in the phase of eating its savings. Worse, as institutions need to adapt to the new situation, reform is hindered by the large voting block of the elderly whose interest lies in the short-term provision of their pensions.

Quite obviously, the current imbalance in the demographic pyramid is the problem. Aoki thinks that fertility must be encouraged. This has worked little in other economies, but may be much easier to implement politically than the best solution, get people to retire later. Immigration is another solution, but as other countries are looking to embrace similar solutions, we may run out of willing young migrants. And Japan is not the obvious choice for a migrant, given the high entry cost in terms of integration.

Option C

In the negotiations over the fiscal cliff, many people think the House Republicans are in a tough spot. The logic is that they have little leverage, because they face only two choices:

A. Concede to most of the president's demands.

B. Take the economy over the cliff, and get blamed for it.

As a result, the logic goes, they will end up doing A, because B is so much worse.

Keith Hennessey points out that there is also option C: Extend the tax cuts, except at the top, for one year. Apparently (and I was not aware of this), Senate Democrats passed a bill doing exactly this back in July. If the House passes it now, it goes to the President's desk, and he would have a hard time vetoing it.

This is not great policy, as it sets up another fiscal cliff one year from now, and it does not address all the spending cuts that are part of the fiscal cliff. But from the Republicans' point of view, it may be better than either A or B. Keith argues that the ability of Speaker Boehner to fall back on this option should give him more bargaining power as he negotiates with the president. That is, because the president won't like option C either, the possibility that it could occur may make him more willing to compromise. From the president's perspective, it is better to make concessions today than having to do this whole fiscal-cliff thing again a year from now.

A. Concede to most of the president's demands.

B. Take the economy over the cliff, and get blamed for it.

As a result, the logic goes, they will end up doing A, because B is so much worse.

Keith Hennessey points out that there is also option C: Extend the tax cuts, except at the top, for one year. Apparently (and I was not aware of this), Senate Democrats passed a bill doing exactly this back in July. If the House passes it now, it goes to the President's desk, and he would have a hard time vetoing it.

This is not great policy, as it sets up another fiscal cliff one year from now, and it does not address all the spending cuts that are part of the fiscal cliff. But from the Republicans' point of view, it may be better than either A or B. Keith argues that the ability of Speaker Boehner to fall back on this option should give him more bargaining power as he negotiates with the president. That is, because the president won't like option C either, the possibility that it could occur may make him more willing to compromise. From the president's perspective, it is better to make concessions today than having to do this whole fiscal-cliff thing again a year from now.

11 Aralık 2012 Salı

The Poverty Trap in France

From Forbes:

Let’s take an unemployed mother living alone with two children between six and 10 years old. In 2010, there were 284,445 French families in this situation that were on welfare.

This mother will be given the “Active Solidarity Income.” Since she has two children, the amount will be $1,100. If she is renting an apartment with a $650 rent, she will be given the “Housing Customized Aid,” amounting to $620. Then she will receive “Family Allowances,” which amounts to another $160. Finally, let’s add the payment known as “Allowance for the start of the school year,” which is $750 once a year, or $62.50 per month. (She might even benefit from other aids, but these are the most common.) She will be given a total of $1,942.50 per month.

Now imagine that this mother has found work and will be paid the “legal minimum wage,” which amounts to $1,820 gross—or $1,430 after taxes. Since she would be earning $1,430, she will no longer receive the “Active Solidarity income.” Her “Housing Customized Aid” will be lowered to $460, but she will still be given “Family Allowances” and the “Allowance for the start of the school year.” Therefore, her total income will amount to $2,112.50....

For this mother of two, working again will bring her family an additional income of only $170. Moreover, this $170 is likely to be lost in the cost of transportation to work, since the cost of gas in France is $7 per gallon. In any case, such a small amount of money is not an incentive to go back to work. Between staying home and working, the choice is simple: welfare is a better deal.

Are immigrant nurses better than domestic ones in the US?

All industrialized economies suffer from a chronic shortage of nurses. Demand for health care is very high, yet nurses are relatively poorly compensated for grueling schedules, important responsibilities and thankless work. It is thus not surprising that the domestic supply of nurses is limited despite major efforts in broadening nursing school opportunities. One has to rely on immigration to fulfill the needs, with potentially the risk of attracting lower quality nurses, as they come from countries with lower human capital and different cultures or traditions.

Patricia Cortés and Jessica Pan study the quality of immigrant nurses and compare them to US native ones using wages and a measure for quality. The half of the nurses migrating to the United States in the last two decades come from the Philippines. They tend to take on harder tasks and tougher schedules (i.e., hospital work), yet they get higher wages than natives even after controlling for education, demographics, location and job characteristics. Non-filipino immigrant nurses fare, however, worse than natives. So is it that Filipinos are that much better? What is certain is that getting educated as a nurse is now done in the Philippines with the explicit goal of emigrating. As green cards for Filipinos are otherwise impossible to obtain (the waiting list is about 40 years long), getting employment sponsorship is essential. I suspect people who would be well qualified for other jobs choose nursing because of the inside track they get for emigration to the US, call that a network effect similar to when entire villages from Italy, Spain or Mexico migrating North for the same occupations, following a few pioneers.

Patricia Cortés and Jessica Pan study the quality of immigrant nurses and compare them to US native ones using wages and a measure for quality. The half of the nurses migrating to the United States in the last two decades come from the Philippines. They tend to take on harder tasks and tougher schedules (i.e., hospital work), yet they get higher wages than natives even after controlling for education, demographics, location and job characteristics. Non-filipino immigrant nurses fare, however, worse than natives. So is it that Filipinos are that much better? What is certain is that getting educated as a nurse is now done in the Philippines with the explicit goal of emigrating. As green cards for Filipinos are otherwise impossible to obtain (the waiting list is about 40 years long), getting employment sponsorship is essential. I suspect people who would be well qualified for other jobs choose nursing because of the inside track they get for emigration to the US, call that a network effect similar to when entire villages from Italy, Spain or Mexico migrating North for the same occupations, following a few pioneers.

10 Aralık 2012 Pazartesi

Unstable matching functions in search theory

The matching function is at the heart of many of labor search models. It has been estimated many times, with a striking empirical regularity: the coefficient that represents matching efficiency appears to decline over time. While it may make sense to see less efficient matching in times of structural change, as it may be happening with the last recession, one would not suspect this over longer samples. Why would labor market performance deteriorate when the information revolution should have reduced matching frictions?

Friedrich Poeschel thinks this is at least in part due to omitted variable bias in the estimation of the matching function. The extant literature relies too much on stocks and neglects various flows, in particular vacancy creation and job seekers beyond the unemployed. Of course, it is not that easy to find such series, or reliable ones. Thus, Poeschel constructs such series from US data using a model of labor market flows. Then, he estimates the matching function using the traditional set variables and then augmenting it with flow variables on the labor supply side. Half of the downward trend in the matching efficiency is taken care of by the new variables. The trend completely disappears once vacancy dynamics are also included. That is reassuring, and maybe one can obtain improving matching efficiency once we get our hands on better data for this.

Friedrich Poeschel thinks this is at least in part due to omitted variable bias in the estimation of the matching function. The extant literature relies too much on stocks and neglects various flows, in particular vacancy creation and job seekers beyond the unemployed. Of course, it is not that easy to find such series, or reliable ones. Thus, Poeschel constructs such series from US data using a model of labor market flows. Then, he estimates the matching function using the traditional set variables and then augmenting it with flow variables on the labor supply side. Half of the downward trend in the matching efficiency is taken care of by the new variables. The trend completely disappears once vacancy dynamics are also included. That is reassuring, and maybe one can obtain improving matching efficiency once we get our hands on better data for this.

9 Aralık 2012 Pazar

Fiscal Cliff Fact of the Day

As reported in the NY Times:

Even if Republicans were to agree to Mr. Obama’s core demand — that the top marginal income rates return to the Clinton-era levels of 36 percent and 39.6 percent after Dec. 31, rather than stay at the Bush-era rates of 33 percent and 35 percent — the additional revenue would be only about a quarter of the $1.6 trillion that Mr. Obama wants to collect over 10 years.

7 Aralık 2012 Cuma

How Japan financed WWII

71 years today, Japan attacked Pearl Harbor and opened a new front in its global war. Why would a relatively small country take on a much larger adversary when it is already stretched with other wars and occupations? In particular, how do you find the resources to wage such wars, and by resources I mean not just the financing but also the physical resources?

Gregg Huff and Shinobu Majima offer part of the answer by looking at the financing of the Japanese occupation of Southeast Asia. Japan had a strategy that invading troops needed to be self-sufficient. This means that they had to either confiscate (tax) or acquire goods through money creation. To a large extend, the latter was performed through the issuance of military scrip, which is unbacked military notes, along with bilateral clearing arrangements with the occupied countries. This allowed not only to finance local occupation but also transfer substantial resources to Japan, in the case of Indochina up to a third of its GDP.

You would think that money creation on such a massive scale would create hyperinflation or at least high inflation. That does not seem to be the case, at least in the sense that the price levels increased as much as the money supply. One could have expected that given the circumstances inflation would have been significantly higher than money growth if market participants were forward-looking and money velocity would increase (think of hyperinflation à la Cagan). Huff and Majima trace this missing hyperinflation to the fact that money was needed to act as a medium of exchange and store of value, despite very substantial seigniorage taxes. There was not viable alternative, in part because of Japanese coercion. I think this would not have worked in more modern economies where more assets are available.

Gregg Huff and Shinobu Majima offer part of the answer by looking at the financing of the Japanese occupation of Southeast Asia. Japan had a strategy that invading troops needed to be self-sufficient. This means that they had to either confiscate (tax) or acquire goods through money creation. To a large extend, the latter was performed through the issuance of military scrip, which is unbacked military notes, along with bilateral clearing arrangements with the occupied countries. This allowed not only to finance local occupation but also transfer substantial resources to Japan, in the case of Indochina up to a third of its GDP.

You would think that money creation on such a massive scale would create hyperinflation or at least high inflation. That does not seem to be the case, at least in the sense that the price levels increased as much as the money supply. One could have expected that given the circumstances inflation would have been significantly higher than money growth if market participants were forward-looking and money velocity would increase (think of hyperinflation à la Cagan). Huff and Majima trace this missing hyperinflation to the fact that money was needed to act as a medium of exchange and store of value, despite very substantial seigniorage taxes. There was not viable alternative, in part because of Japanese coercion. I think this would not have worked in more modern economies where more assets are available.

6 Aralık 2012 Perşembe

Good weather and absenteeism

Ah, the weather is so nice outside, yet I am stuck inside working. If only I could take a vacation day. But wait, I could declare myself sick for a day, would not need a doctor's note because it is just a day, and enjoy life! Well, this is not that easy in my case, as I still need to get the work done, but the temptation is there. And many likely cross that line.

Jingye Shi and Mikal Skuterud use absenteeism data for Canada and find indeed that good weather encourages people to take sick leaves. Given the harsh winter climate in Canada, they limit the analysis to non-winter months and indoor workers, so that the temptations are maximized. Yes, they find that short-term "sickness" increases with good weather, but strangely it affects more workers who do not enjoy sick pay benefits or are on probation. The authors suggest this is because they cannot capture some implicit agreement that one can use short sick leaves for other purposes. That does not convince me.

Jingye Shi and Mikal Skuterud use absenteeism data for Canada and find indeed that good weather encourages people to take sick leaves. Given the harsh winter climate in Canada, they limit the analysis to non-winter months and indoor workers, so that the temptations are maximized. Yes, they find that short-term "sickness" increases with good weather, but strangely it affects more workers who do not enjoy sick pay benefits or are on probation. The authors suggest this is because they cannot capture some implicit agreement that one can use short sick leaves for other purposes. That does not convince me.

5 Aralık 2012 Çarşamba

An Unfortunate Broken Promise

Back in 2008, when President Obama was running for his first term, he promised to be a post-partisan leader. While a Democrat, he said he would accept good ideas when they came from Republicans. At the time, I believed him, at least to some degree. And I wrote about it in this NY Times column.

Sadly, I was wrong. The short version of the story is this: As a candidate, President Obama campaigned on a platform of raising taxes on the rich. Yet he and his economic advisers also said they wanted to raise dividend taxes only slightly, from 15 to 20 percent. For reasons I explained in the Times article, keeping dividend taxes low was a position bolstered by good economics. Now, however, the president wants to raise dividend taxes to ordinary income tax rates (plus, for high-income taxpayers, the new tax of 3.8 percent that is part of the Obamacare legislation).

To put it another way, he campaigned as a moderate, willing to concede that the other party had some good ideas on tax policy. Once in office, he gave up on those ideas.

A similar thing happened with Bowles-Simpson. During his first term, he appointed a bipartisan panel, which concluded we could address our long-term fiscal problem with lower tax rates and a broader tax base. Now, the President goes around the country lambasting that approach.

Reasonable people can disagree about whether President Obama is a good or bad president. But the claim that he has tried to transcend partisanship and find a middle ground is just impossible to square with the facts.

Sadly, I was wrong. The short version of the story is this: As a candidate, President Obama campaigned on a platform of raising taxes on the rich. Yet he and his economic advisers also said they wanted to raise dividend taxes only slightly, from 15 to 20 percent. For reasons I explained in the Times article, keeping dividend taxes low was a position bolstered by good economics. Now, however, the president wants to raise dividend taxes to ordinary income tax rates (plus, for high-income taxpayers, the new tax of 3.8 percent that is part of the Obamacare legislation).

To put it another way, he campaigned as a moderate, willing to concede that the other party had some good ideas on tax policy. Once in office, he gave up on those ideas.

A similar thing happened with Bowles-Simpson. During his first term, he appointed a bipartisan panel, which concluded we could address our long-term fiscal problem with lower tax rates and a broader tax base. Now, the President goes around the country lambasting that approach.

Reasonable people can disagree about whether President Obama is a good or bad president. But the claim that he has tried to transcend partisanship and find a middle ground is just impossible to square with the facts.

Longevity increased much before the Industrial Revolution

There is no doubt that average human lifetimes have considerably lengthened since Antiquity (except, maybe, Biblical times...). Improvements in living standards through better nutrition, salubrity and medicine likely were the major factors in this dramatic evolution. When this improvements started kicking in is a subject of debate, which is not helped by the fact that good data about lifetimes is difficult to come by. Written genealogical records go only so far back, and their quality and comprehensiveness declines considerably with age. And working from cemeteries is also quite unreliable, especially for longer horizons.

David de la Croix and Omar Licandro provide a very significant step towards a better understand of longevity in human history by compiling a database of 300,000 famous people spanning 25 centuries. The data includes information about location, religion, occupation, and nationality, which should take care of the major selection biases. They find that longevity was mostly flat throughout human history until it started increasing with the cohort born in the 1640s. This is before Malthus, whose assumption of stagnation is thus wrong. And this is much before the Industrial Revolution and has happened across the world and across occupations, thus the two events seem unrelated.

David de la Croix and Omar Licandro provide a very significant step towards a better understand of longevity in human history by compiling a database of 300,000 famous people spanning 25 centuries. The data includes information about location, religion, occupation, and nationality, which should take care of the major selection biases. They find that longevity was mostly flat throughout human history until it started increasing with the cohort born in the 1640s. This is before Malthus, whose assumption of stagnation is thus wrong. And this is much before the Industrial Revolution and has happened across the world and across occupations, thus the two events seem unrelated.

4 Aralık 2012 Salı

Are smart meters worth it?

Smart meters that allow you to monitor and manage electricity consumption are all the rage now. Power companies push them to consumers as the best deal that has ever been offered. And it looks enticing, as it promised more flexibility and the possibility of applying peak pricing in areas where this is not yet current. But is there really that much to gain? After all, these meters are not inexpensive technology.

Thomas-Olivier Léautier helps us here. He estimates how the responses of French households would be once they have smart meters and they can adjust their consumption to market prices. The outcome is humbling: the yearly savings would amount to 1-4€, which is likely less than forgetting to close a window one day in winter and much less than the 25 &euro/year cost of a smart meter. I see two reasons for this result. First, most households consume little energy. Second, their consumption pattern is not that flexible.

But would this result extend to other countries? North American households use a lot more electricity than French households due harsher climates and more carelessness about energy consumption. A smart meter there may in particular make people more aware of their power consumption and how one can reduce it to save money. This is much like a car that shows current gas consumption entices the driver to use less fuel. And this effect may make it worth it.

Thomas-Olivier Léautier helps us here. He estimates how the responses of French households would be once they have smart meters and they can adjust their consumption to market prices. The outcome is humbling: the yearly savings would amount to 1-4€, which is likely less than forgetting to close a window one day in winter and much less than the 25 &euro/year cost of a smart meter. I see two reasons for this result. First, most households consume little energy. Second, their consumption pattern is not that flexible.

But would this result extend to other countries? North American households use a lot more electricity than French households due harsher climates and more carelessness about energy consumption. A smart meter there may in particular make people more aware of their power consumption and how one can reduce it to save money. This is much like a car that shows current gas consumption entices the driver to use less fuel. And this effect may make it worth it.

3 Aralık 2012 Pazartesi

A Reading for the Pigou Club

From The New Yorker. One disappointing quotation:

"We would never propose a carbon tax, and have no intention of proposing one," [White House spokesman Jay] Carney told reporters.

Dealing with congestion: fast lane or toll booth?

In densely populated areas, road congestion is a fact of life. As time lost in traffic has an economic value, it is then quite obvious that road pricing with flexible tolls that depend on the current level of demand should provide for the most efficient allocation of cars through time and space. But there are some logistic problems with this, and depending on the actual implementation, some privacy issues as well.

Mogens Fosgerau claims one can get a Pareto improvement with a toll lane that is reserved for particular users if demand is inelastic. The lane set-up is similar to airport check-in, where privileged people get their own lane and others can use it if it is available. I question, though, that demand is inelastic. That may well be the case in the short-run, but people do adapt to road prices on a longer horizon by changing schedules and locations. Also, I find the comparison to tolls unfair in the sense that the benchmark is a coarse toll: there is a single toll price that is only activate when there is congestion. Obviously, it creates peak loads right before and after it is in place. That can easily be improved with more flexible pricing.

Mogens Fosgerau claims one can get a Pareto improvement with a toll lane that is reserved for particular users if demand is inelastic. The lane set-up is similar to airport check-in, where privileged people get their own lane and others can use it if it is available. I question, though, that demand is inelastic. That may well be the case in the short-run, but people do adapt to road prices on a longer horizon by changing schedules and locations. Also, I find the comparison to tolls unfair in the sense that the benchmark is a coarse toll: there is a single toll price that is only activate when there is congestion. Obviously, it creates peak loads right before and after it is in place. That can easily be improved with more flexible pricing.

Some Advice on Tax Planning

I don't normally give advice on personal finances, but in light of the fiscal situation we are facing, I will pass along one tidbit. Consider converting some of your retirement savings into a Roth IRA. Over the past few years, I have converted all that I can, which is about half of my retirement savings.

To make the best of a Roth conversion, you need liquid assets outside of retirement accounts to pay the resulting tax liability. But if you can do this, you will shelter more of your savings from capital taxation, and you will avoid required minimum distributions when you turn 70 1/2, which means tax-free accumulation for a longer period of time.

To read more about this option, click here.

To make the best of a Roth conversion, you need liquid assets outside of retirement accounts to pay the resulting tax liability. But if you can do this, you will shelter more of your savings from capital taxation, and you will avoid required minimum distributions when you turn 70 1/2, which means tax-free accumulation for a longer period of time.

To read more about this option, click here.

1 Aralık 2012 Cumartesi

Why the President is Not So Keen on Just Limiting Deductions

From the White House blog. Bottom line: If you apply a $25,000 deduction cap only to households with income above $250K, phase in the cap gradually as income rises above $250K, and exclude charitible giving from the cap, you increase revenue by only $450 billion over ten years.

30 Kasım 2012 Cuma

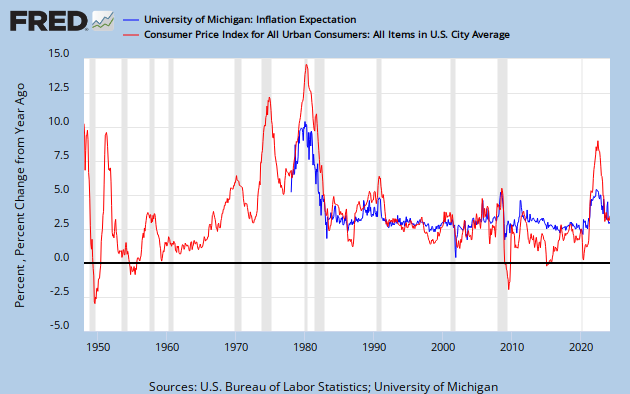

Inflation expectations and rational behavior

Ask people on the street (à 24-hour news channel that needs to fill time) about the inflation rate, and I am quite sure you get an very upward biased estimate. Or at least this is what I would have expected, but the data seems to contradict me: comparing US inflation expectations from the University of Michigan Consumer Survey and the realized CPI, there is no obvious bias visible, meaning they seem to have rational expectations:

However, are these consumers rational all the way, that is, do their actions follow their expectations? Olivier Armantier, Wändi Bruine de Bruin, Giorgio Topa, Wilbert van der Klaauw and Basit Zafar design an experiment where payoffs depend on future inflation. By and large, participants seems to act in a way that is consistent both qualitatively and quantitatively with expect utility theory. The only ones that stray away and not surprisingly less educated consumers, but their impact is rather small (in numbers, and me now that zero-intelligence traders have no impact on markets). My faith in the US consumer is restored.

However, are these consumers rational all the way, that is, do their actions follow their expectations? Olivier Armantier, Wändi Bruine de Bruin, Giorgio Topa, Wilbert van der Klaauw and Basit Zafar design an experiment where payoffs depend on future inflation. By and large, participants seems to act in a way that is consistent both qualitatively and quantitatively with expect utility theory. The only ones that stray away and not surprisingly less educated consumers, but their impact is rather small (in numbers, and me now that zero-intelligence traders have no impact on markets). My faith in the US consumer is restored.

The Gray Lady's Misleading Headline

Over my coffee this morning, I read the following headline on the front page of The New York Times: "Complaints Aside, Most Face Lower Tax Burden Than in the Reagan ’80s." Below it was a graphic comparing average tax rates for various income groups in 1980 and 2010.

The problem is that Reagan did not become president until January 1981, and his tax policy was not fully implemented until a couple of years later (and arguably not until his second term, when we got very significant tax reform). So the headline should have read, "Complaints Aside, Most Face Lower Tax Burden Than in Carter's 1980." That makes the story very different, as 1980 was the year the incumbent Carter was defeated by the challenger Reagan, who was proposing significant tax reduction as a key part of his campaign.

By the way, the online version of The Times omits the mention of Reagan in the headline. There, the headline is the more accurate "Complaints Aside, Most Face Lower Tax Burden Than in 1980."