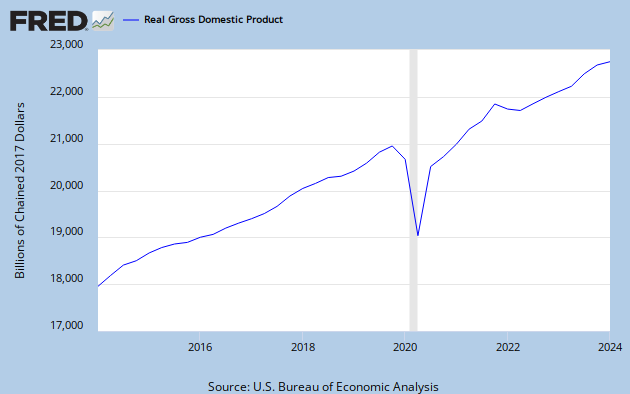

Fiscal policy being in complete disarray and unpredictable in the United Sates, economic policy is currently limited to monetary policy. But even there, it is not blindingly obvious what the Federal Reserve should do. If economic activity is below potential (and is forecasted to remain so beyond the "long and variable lags" it takes for monetary action to have an impact), the monetary easing is in order. Define potential, and there disagreement starts. If you look at the evolution of GDP, you cannot help thinking that it went through a permanent downward shift and is now tugging along at the usual growth rate, simply a step below. This would mean we are ready to get off the zero interest rates:

That would go against the idea that there are no permanent shifts in GDP. But while there are usually no such shifts, maybe there are rare circumstances where they happen. Mehdi Hosseinkouchack and Maik Wolters test the unit root of US GDP not only at the conditional mean but also at the tails of the distribution using a quantile autoregression based unit root test. Ad they find that sharp declines in output, like the one we recently experienced, do indeed look permanent. We should therefore not expect GDP to get on the previous path, and this not treat the latter as our current potential GDP. Would the FOMC believe this? I doubt it.

That would go against the idea that there are no permanent shifts in GDP. But while there are usually no such shifts, maybe there are rare circumstances where they happen. Mehdi Hosseinkouchack and Maik Wolters test the unit root of US GDP not only at the conditional mean but also at the tails of the distribution using a quantile autoregression based unit root test. Ad they find that sharp declines in output, like the one we recently experienced, do indeed look permanent. We should therefore not expect GDP to get on the previous path, and this not treat the latter as our current potential GDP. Would the FOMC believe this? I doubt it.

Hiç yorum yok:

Yorum Gönder